- By Sheldon Kimber, CEO, Intersect Power

The climate is warming and our society will be forced to decarbonize well beyond the power sector. That much is certain, and just a matter of time. At the same time, clean electricity is reaching unprecedented levels of affordability and availability, and not all of it can or should find its way onto the power grid. I believe that the combination of these two factors will result in exponential growth in Five Inevitable Industries that have the potential to get the planet to net zero emissions on their own, without massive new breakthroughs.

I’ve been discussing this for the past few years, but I finally got around to writing it down. What follows is a five part thesis covering one potential view of our low carbon future, an overview of the important dynamics that dictate the direction of this transition, and some discussion of who might benefit and how.

Others may have written about distinct pieces of this overarching vision, but I think Intersect has a uniquely bold and cohesive vision combined with a team that knows what it takes to build physical infrastructure at this scale. My hope is that you find this as inspiring and hopeful as I do. I hope it leaves you optimistic that there is in fact a path to solving the climate crisis with well understood technologies being deployed at a much larger scale in different areas of the economy than before. This is the vision that keeps me coming into work every day and allows me to tell my kids that there is a path forward for their generation.

PART ONE: Business Plans Are Easy When You Know The Future

I have several basic but useful questions that I’ve used to frame business decisions and strategy. One day I’ll write a really boring business book with a chapter for each, but until then you’ll have to settle for this blog, which covers what I think is the most useful one of the bunch.

This key question is, “Given the current state of the market, are there any future outcomes that are likely to occur in almost any future state?” Or, in short, “Are there any inevitabilities?”

It’s rarely possible to predict specific events or exactly when things might happen, but it’s been surprisingly easy to spot larger trends that are sure to happen over a long time horizon. It’s served me well as I’ve bet on the unavoidable rise in the value of clean energy and the unstoppable cost declines brought about by learning curves in clean technologies. These were both fairly obvious trends starting in the mid 2000’s, and today underlie the success of multi-billion dollar companies and some of the fastest growing industries on earth.

A global response to climate change is inevitable, and the resulting economic changes are fairly obvious if you look closely enough. I am not going to attempt to guess when the planet will respond, nor to speculate on how much irreversible damage will have been done by that point. I am simply pointing out that climate change doesn’t stop at 1.5 degrees. It keeps going, with ever more cataclysmic consequences such that even the most stubbornly ignorant defenders of the status quo will eventually be begging for zero carbon alternatives.

This conjecture leads to some pretty simple conclusions about our future state.

- Carbon will eventually have a price.

- Only multi-gigaton solutions really matter.

- Value will be increasingly concentrated in the green attributes of certain products, not the products themselves.

- Negative emissions technologies will be required.

- Retrofitting and reuse of current infrastructure must be a large part of the solution.

- Large scale adaptation is unavoidable.

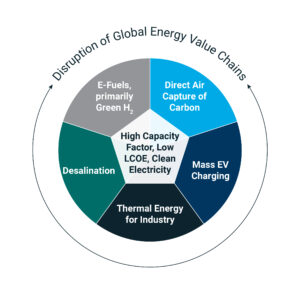

There’s a lot to unpack in each of these. For now I’m focused on what we can intuit about the economy in this future state, because defining a business strategy is far easier when you know the future, or at least a rough approximation of it. In the future state we have defined above, we are likely to see the emergence of several trillion dollar industries that simply don’t exist today. I call these the Five Inevitable Industries and they are listed below.

- Green Hydrogen and E-Fuels

- Direct Air Capture

- Electrification of Industrial Thermal Loads

- Mass EV Charging

- Desalination and Water Transportation

It may be that only a couple ever make it to scale, or that others emerge that are not on this list. But I think that counting on the emergence of these five industries is a good bet relative to other prognostications you could make about our zero carbon future.

Why are these the ones? Because these are based primarily on what MUST happen, what is inevitable. And what makes them inevitable is:

- They are massively scalable, benefiting from economies of scale both within their supply chain and also within each installation.

- They leverage existing technologies relying only on the well understood learning curves that come with mass deployment.

- They benefit from the rapid improvement of adjacent technologies, such as wind and solar.

- The entrenched political and business interests are least threatened by and likely to see the most opportunity for themselves in these new industries.

- These industries have the ability to reuse or retrofit large portions of today’s industrial and energy infrastructure with dramatically reduced carbon emissions.

- Together they are sufficient to all but solve our climate problem.

Are there better solutions? It depends who you ask. There are many other values by which you can measure our response to climate change and by extension judge these solutions. When I say these are inevitable it is based on what I see as the current set of facts on the ground and the singular value of stopping emissions before it is too late.

None of these will satisfy the type of values-based advocacy or narrow efficiency arguments that lead you down the road of rooftop solar, the unlikely permitting of a massive number of new nukes, catching cow farts, or simply demanding that everyone stop driving and consuming. Don’t get me wrong, I’m still an all-of-the-above guy and some of these alternatives are things I wish would happen based on my own values, but if you’re predicting the trillion dollar industries of tomorrow, these will not be them.

Perhaps the most telling predictor of these Five Inevitable Industries is what they have in common. More on that in the next installment.

PART TWO: High Capacity Factor, Low Cost, Clean Electricity is The Nexus Of Deep Decarbonization

So what do all of the Five Inevitable Industries have in common? First, they are each currently available technologies that are being made cost effective by the increasing abundance of high capacity factor, low-cost, clean electricity. The extraordinary cost declines in renewable electricity allow us to leverage the sector in which we have made the most progress in the past two decades to decarbonize the rest of our society.

High Capacity Factor, Low LCOE, Clean Electricity in the Nexus of Deep Decarbonization

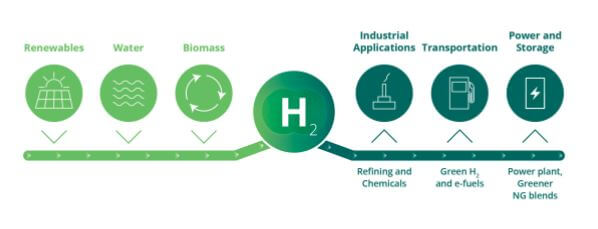

Green Hydrogen and E-fuels are perhaps the most advanced, or at least the most talked about, of these industries. While all of these trends are driven by the fact that carbon will be priced either directly (or indirectly through tax credits, etc) and multi-gigaton solutions will be prioritized, Green Hydrogen and E-fuels are further driven by the need for the retrofit and reuse of current infrastructure.

Green Hydrogen and E-fuels are perhaps the most advanced, or at least the most talked about, of these industries. While all of these trends are driven by the fact that carbon will be priced either directly (or indirectly through tax credits, etc) and multi-gigaton solutions will be prioritized, Green Hydrogen and E-fuels are further driven by the need for the retrofit and reuse of current infrastructure.

The capital expenditure and time required to replace all carbon intensive infrastructure in the necessary time frame is prohibitive. If we wait for all airplane engines, gas turbines, industrial boilers, steel mills, ships and other existing infrastructure to be replaced, it will be too late. Infrastructure is persistent , especially broadly distributed infrastructure like airplane engines that are point sources individually, but make up a massive emissions source collectively. These are far harder to swap out than utility scale power plants which are far more centralized sources of carbon emissions.

Moreover, liquid and gaseous fuels have an energy density, storage properties and other flexibility that make them far more valuable than electrons on a wire. Arguments about things like “well to wheel efficiency” of green hydrogen will fall away as it becomes clear that input energy is cheap enough, and the flexibility premium of liquid and gaseous fuels in certain applications is high enough, to make overall efficiency less relevant. We’ll see this in applications such as aviation, but also in certain industries such as the manufacture of steel and cement that require fuels capable of producing heat and steam at a quality that electrification cannot meet in the near term.

Simply put, the transition will require zero carbon fuels that are “drop in” replacements for hydrocarbons.

But net zero will not be achievable in all sectors and even if it is, by that point net zero will no longer be enough. Negative emissions solutions will be required.

Today’s direct air capture technologies are “too expensive” partly due to their energy intensity. It takes massive amounts of energy to fuel the chemical processes that capture and sequester carbon from the atmosphere. Luckily, we have an increasing amount of high capacity factor, low-cost, clean electricity to fuel such processes, and this is enabling the first large scale projects to become feasible. As these projects are built and we come down the learning curve on direct air capture technology, the cost of these facilities will fall, allowing them to run on energy that may have a lower capacity factor or be slightly more expensive. This will increase the geographic footprint over which these technologies can compete in much the same way that renewables have done in the past two decades. It’s important to note that this virtuous cycle of declining costs allowing for lower capacity factors or more expensive clean energy inputs is a characteristic of almost all of our Five Inevitable Industries.

Direct air capture will likely be the “backstop” technology for carbon abatement against which most other solutions are measured. For instance, if you can take carbon out of the atmosphere for $200/ton, a solution to stop carbon from being put into the atmosphere will need to be less than $200/ton to make sense. Even if a technology is slightly more expensive than this “backstop” price, the limits of underground storage and hesitancy of environmentalists to accept sequestration as a permanent solution will likely keep direct air capture from displacing other efforts to decarbonize the economy. Instead it will allow us more time to advance green hydrogen, clean steel and other zero carbon solutions and potentially provide a mechanism to undo some of the damage that we have already done.

Currently, 30% of all carbon emissions come from industrial loads, 2/3 of which are produced from boiling water. That’s a gross oversimplification, but not too far off the mark. Our economy consumes huge amounts of steam for various industrial processes. Much of this steam is produced in boilers or cogeneration of some type using fossil fuels, mostly natural gas. When most folks think of “electrification” they think of cities like Berkeley, CA, ripping up the gas distribution system and demanding that everyone use an induction stove, but that approach and the high profile controversy surrounding it are the rooftop solar of thermal electrification. In other words, highly visible, unevenly distributed and the subject of endless debate but ultimately not of sufficient scale to matter over the given time horizon.

What will truly move the needle is finding ways to electrify the production of steam or the baking, drying, melting and similar direct heating processes found in large industrial facilities. If the decarbonization of these loads is inevitable it is almost certain that large portions of that work will need to be done with either electric boilers powered with low cost, high capacity factor, clean electricity or using green hydrogen and e-fuels made from that same input.

Technologies that exist today can likely address much of this market for clean industrial thermal loads. Electric boilers and similar technologies can already provide steam at adequate pressures and temperatures to address large portions of this market. The typical refrain of electric solutions not being able to meet the quality needs of this market is limited to a few specific applications, leaving a huge majority of this market open to electrification. In fact, even those high temperature applications can be electrified by substituting green hydrogen or other fuels made from clean electricity for the fossil fuels currently in use.

This market in particular will require high capacity factor electricity or efficient storage of thermal energy as many steam loads are continuous and interruptions will be costly to the industrial processes that they support. This is a recurring theme throughout the Five Inevitable Industries and why I’m so pedantic about referring not just to clean energy but to low cost, high capacity factor, clean electricity.

PART THREE: Who Makes The Gas Pump? Who Makes The Gasoline? Which One Have You Heard Of?

So far we’ve hit on three of the Five Inevitable Industries – Green Hydrogen and E-fuels, Direct Air Capture and Thermal Electrification. These industries barely exist today, unlike electric vehicles which many believe are already on their way to mass adoption. But EV charging as we know it is in its infancy. As we move toward aggregated or mass EV charging as I’ve sometimes referred to it, we move beyond pleasant software interfaces and chargers that look like gas pumps. We are going to need distribution grid upgrades to go from having 5-10 chargers in the corner of a mall parking lot to electrifying a significant percentage of the entire parking garage. When this change occurs, EV charging is at least as much about the deployment of massive utility scale infrastructure as it is about charging networks, member growth, network effects and software.

Highly capital-intensive assets will need to be deployed with a combination of expertise in electric power, real estate, finance and wholesale power markets. Aggregated charging loads will increasingly participate in wholesale power markets as both loads and storage assets. Billions of dollars worth of distribution-level storage assets will need to be deployed, financed and optimized to buffer each mass charging site. Gigawatt hours of high capacity factor, low cost, clean electricity will need to be procured to meet a constantly shifting load curve. This procurement will be done in power markets that are also undergoing massive volatility and change as they accept more renewable generation, storage assets and demand shocks from electrification of other sectors.

In short, a trillion dollar market with a capital intensive and complex upstream supply chain must manifest where until just recently there was nothing.

The big question within this Inevitable Industry is who will win. The obvious answer here is the charging network companies, fresh off their respective SPACs and investing like crazy in their own networks. But dig a little deeper and ask yourself whether the functions above – asset finance, development and managing massive and dynamic demand for clean energy — are core competencies for any of these companies.

It is far more likely that the charging networks will expand by bundling services and other innovative marketing focused on network growth than by vertically integrating back upstream into hard infrastructure. For a long time, I had assumed that the utilities would dominate this space with investments in distribution level infrastructure, large scale grid edge storage, charging tariffs and the like. However, the speed with which the utilities are moving does not give me confidence that they will get there in time. This leaves a massive market without a clear winner.

The scale of energy demand and delivery that will eventually result from these massive charging networks will be like nothing the grid has ever seen. Making good on the promise of the EV revolution is at least as much about building, financing, managing and dispatching utility scale infrastructure assets as it is about the cars themselves. This is why I believe that the inevitable switch to EVs and the associated need for aggregated EV charging depends on the generation and delivery of massive amounts of high capacity factor, low cost electricity, and those with expertise in this area will be ideally situated to capture value in the eventual trillion dollar EV charging market of the next few decades.

PART FOUR: The Future of Water Is Clean Energy

So far we’ve focused on the rise of technologies that will solve the climate crisis and eliminate our emissions problem. The final Inevitable Industry that I see emerging is a little different in that it is not a solution focused on emissions reduction, but rather an inevitable adaptation that our society will be forced to make.

Access to clean, fresh water will be one of the largest challenges of climate change. Large portions of the world will lose reliable access to water for purposes of drinking, irrigation, sanitation and industry. Desalination and transportation technologies turn the water problem into an energy problem. That doesn’t necessarily solve the water problem, but in a world increasingly awash in abundant clean electricity, it gives us a pathway to convert the 97% of water on earth that is not potable into drinkable and usable water and move it to where it is most needed.

Desalination is a proven technology but it is highly energy intensive and still has a relatively high capital cost. This fits the exact profile of the other Inevitable Industries, allowing desalination to at first be enabled by broadly available low cost, high capacity factor, clean electricity. Eventually, once the cost has declined with mass deployment of desalination equipment, broadening the footprint where desalination can be economical to areas where high capacity factor, clean electricity may be a little more costly.

Water transportation doesn’t exhibit quite the same dynamic, but it is worth mentioning as water pumping loads already consume massive amounts of electricity in places like the American West where water is moved in large volumes for use in agriculture. And such large volume, long distance transport will only increase as the world seeks to distribute desalinated water or surface water from places that remain wet to places that are seeing decreasing water supplies.

PART FIVE: Industrial Scale Behind-The-Meter and The Remaking Of Retail Energy

As I wrap up this five part series on the Nexus of Deep Decarbonization and Intersect Power’s vision for a low carbon economy there is one open question with regard to all of these Inevitable Industries that I think is worth addressing. The location of these Five Inevitable Industries goes to the heart of how they will develop and who will benefit from this green industrial revolution.

Will we see electricity, green hydrogen or other energy carriers delivered over existing infrastructure to current industrial centers where these new industries will take root? Will we see “industrial scale” behind-the-meter renewables with less favorable levelized costs of electricity closer-in to existing industrial centers, thereby paying a little more for clean energy but avoiding the costs of grid delivery? Or will we actually see the realignment of the entire industrial economy with many of these new clean loads choosing to site in areas where they can access behind-the-meter renewables or otherwise cheaper grid-delivered clean energy?

I think it will be a combination of all three of these things. But one thing is clear, as a significant portion of our existing and emerging economy requires electrification, it will be a jump-ball between gas infrastructure, which currently serves much of this load, electricity infrastructure, and behind-the-meter alternatives to see who can deliver cost-effective solutions for this massive change in industrial energy usage.

The outcome of this free-for-all will dictate which entities own the customer relationships across the energy industry and might even upend the regulatory structures in today’s markets. This is the final element of the Five Inevitable Industries – massive disruption of the utility and retail energy business model. This is not what I think of as one of the Inevitable Industries per se, but more of a knock-on effect of these Inevitable Industries. If low cost, high capacity factor, clean electricity is the nexus which links and enables the Five Inevitable Industries, then the disruption of today’s midstream and downstream business models is the consequence of the realignment in energy demand that will come about as these Inevitable Industries scale.

By now you’re tired of hearing it, but all of the above can be simplified down to the following: High capacity factor, low cost, clean electricity is the Nexus of Deep Decarbonization.

It is the enabling factor that “turns on” these new zero carbon, trillion dollar industries. It will enable them to deploy at scale and come down the cost curve for their own capex, enabling them to buy more clean electricity and likely reducing the cost of that electricity further by bringing renewable generation technologies even further down their own learning curve. This virtuous cycle of demand and scale is the greatest hope we have for solving the climate crisis.

As a species, we are susceptible to a whole host of inconvenient traits including selfishness, mass delusions and the emotional desire to feel like an important part of an accepted group or something greater than ourselves. These things divide us today even more so than they have in recent human history. But as humans, we are also distinguished by our survival instinct, our capacity for innovation and our compassion for others who suffer. I choose to believe that it will be these last three traits that ultimately define our response to climate change. Because of this I cannot imagine a future where we fail to address this crisis. If my optimism is correct, then there is ample reason to believe that a large portion of the foregoing is, in fact, inevitable.